Research

FEB 2024, R&R Review of Financial Studies

With: Arpit Gupta and Sabrina Howell (NYU Stern)

Aug. 2025, Journal of Finance

With: Jun Chen (Univ. of IL, Chicago)

July 2024, Journal of Finance

With:

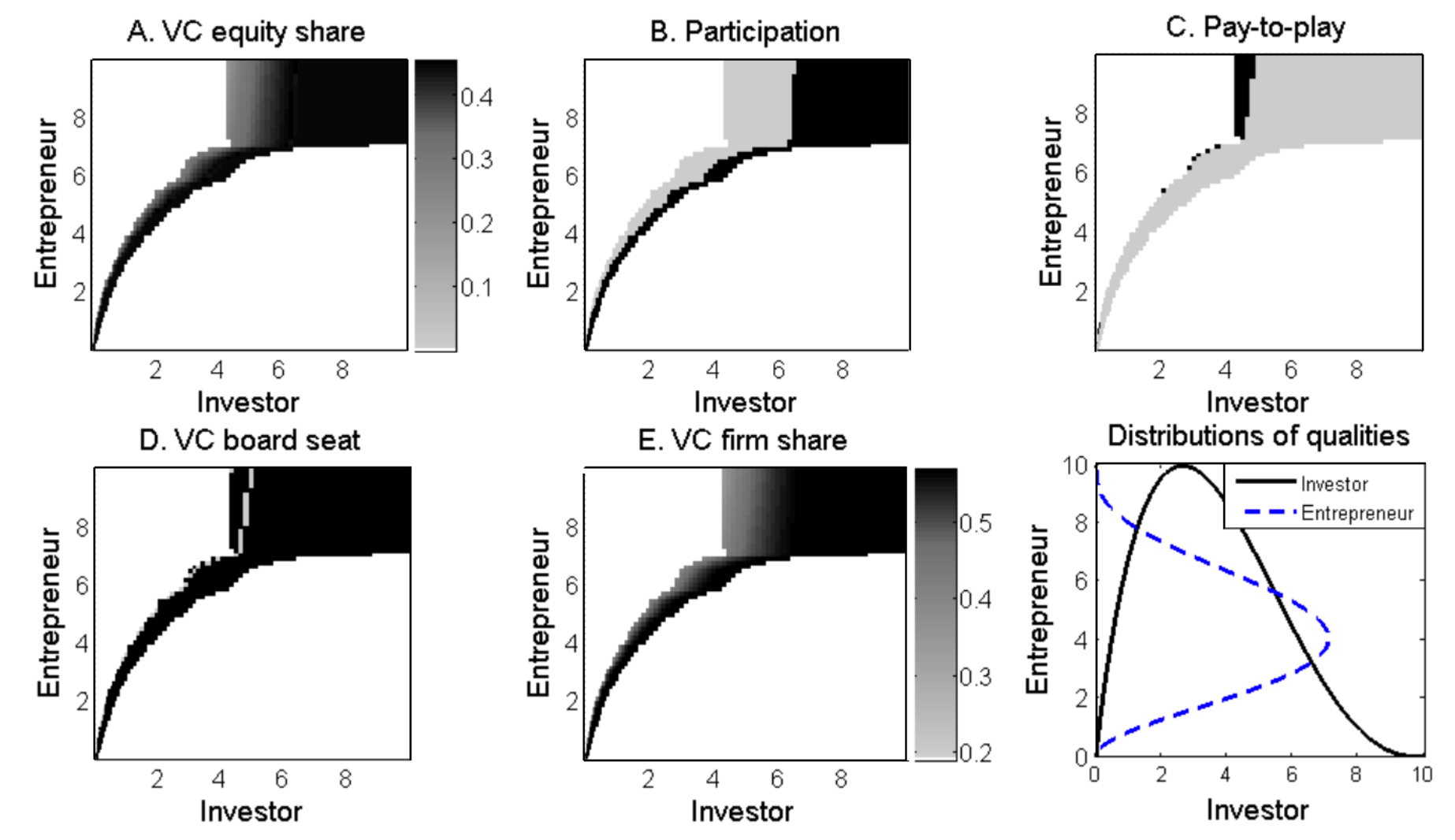

Nadya Malenko (Boston College)

Sept 2023, Management Science

With:

Ryan Peters (Tulane) and Sean Wang (SMU)

November 2023, Journal of Financial Economics

With:

Kairong Xiao (Columbia) and Ting Xu (Univ. of Toronto)

Aug. 2024, Journal of Finance

With:

Ramana Nanda (Imperial) and Christopher Stanton (HBS)

February 2023, Handbook of the Economics of Corporate Finance

Fall 2022, Annual Review of Financial Economics

With: Joan Farre-Mensa (Univ. of IL, Chicago)

March 2021, Forthcoming Journal of Financial Economics

With:

Alexander Gorbenko (UCL) and Arthur Korteweg (USC)

2020, Review of Financial Studies (Editor’s Choice)

With:

Joan Farre-Mensa (Univ. of IL Chicago)

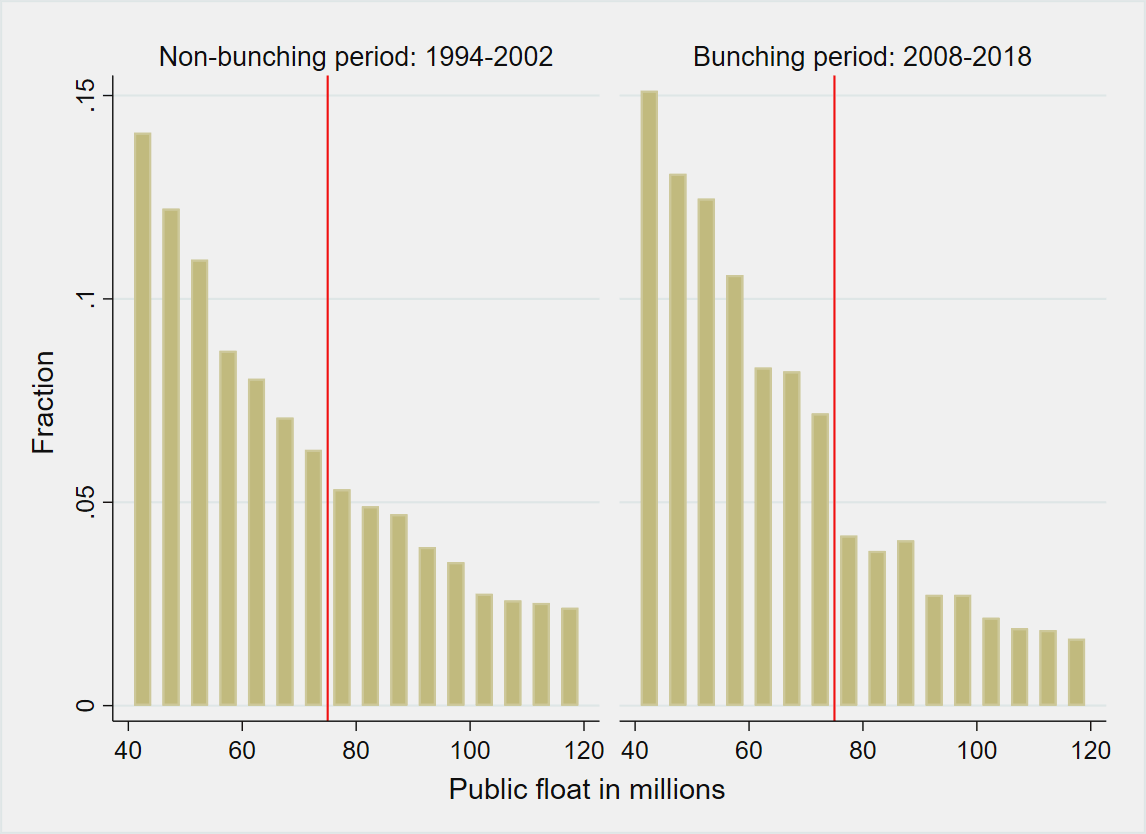

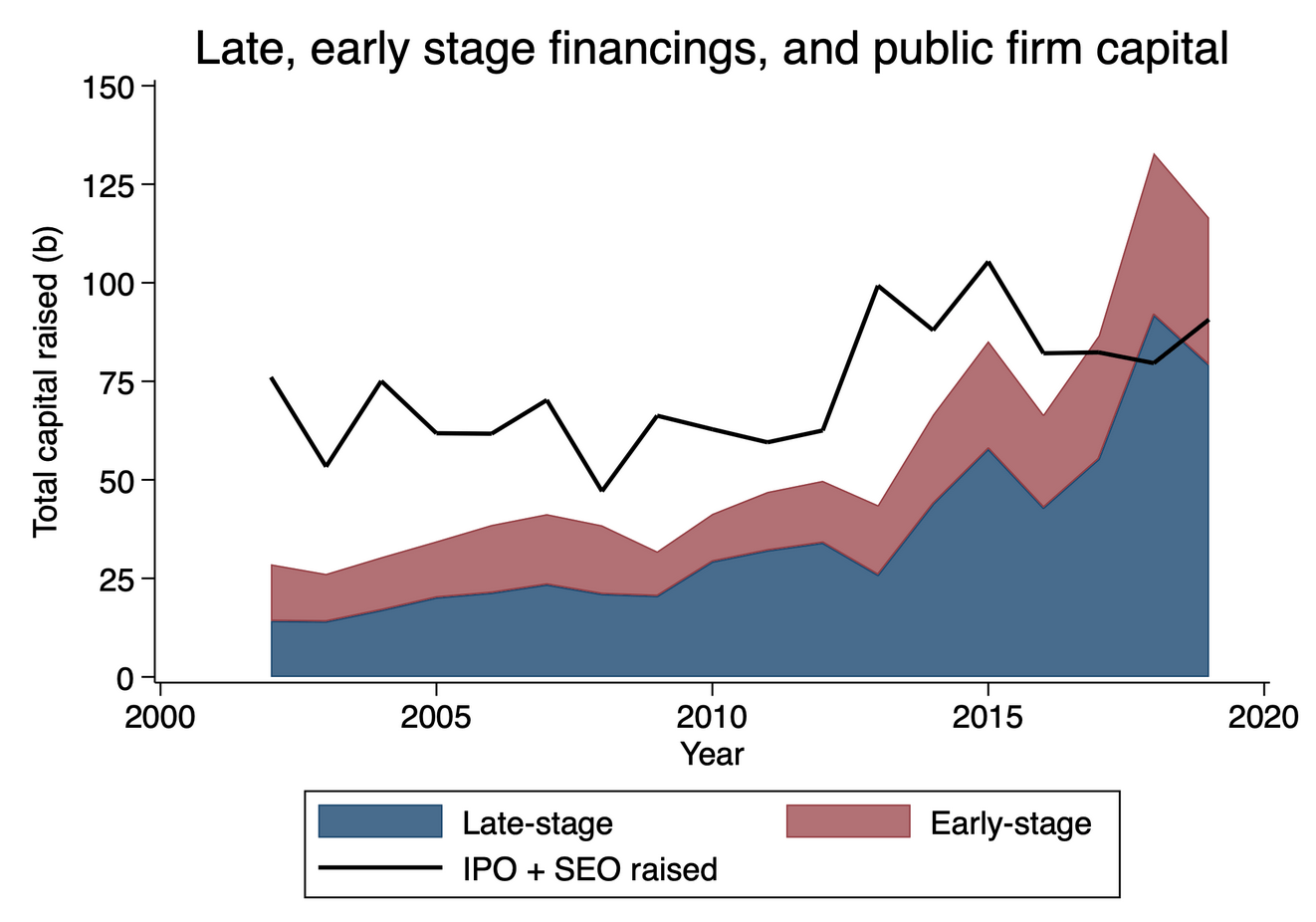

The deregulation of securities laws|in particular the National Securities Markets Improvement Act (NSMIA) of 1996|has increased the supply of private capital to late-stage private startups, which are now able to grow to a size that few private firms used to reach. NSMIA is one of a number of factors that have changed the going-public versus staying-private trade-off, helping bring about a new equilibrium where fewer startups go public, and those that do are older. This new equilibrium does not reflect an IPO market failure. Rather, founders are using their increased bargaining power vis-a-vis investors to stay private longer.

2020, Journal of Financial Economics

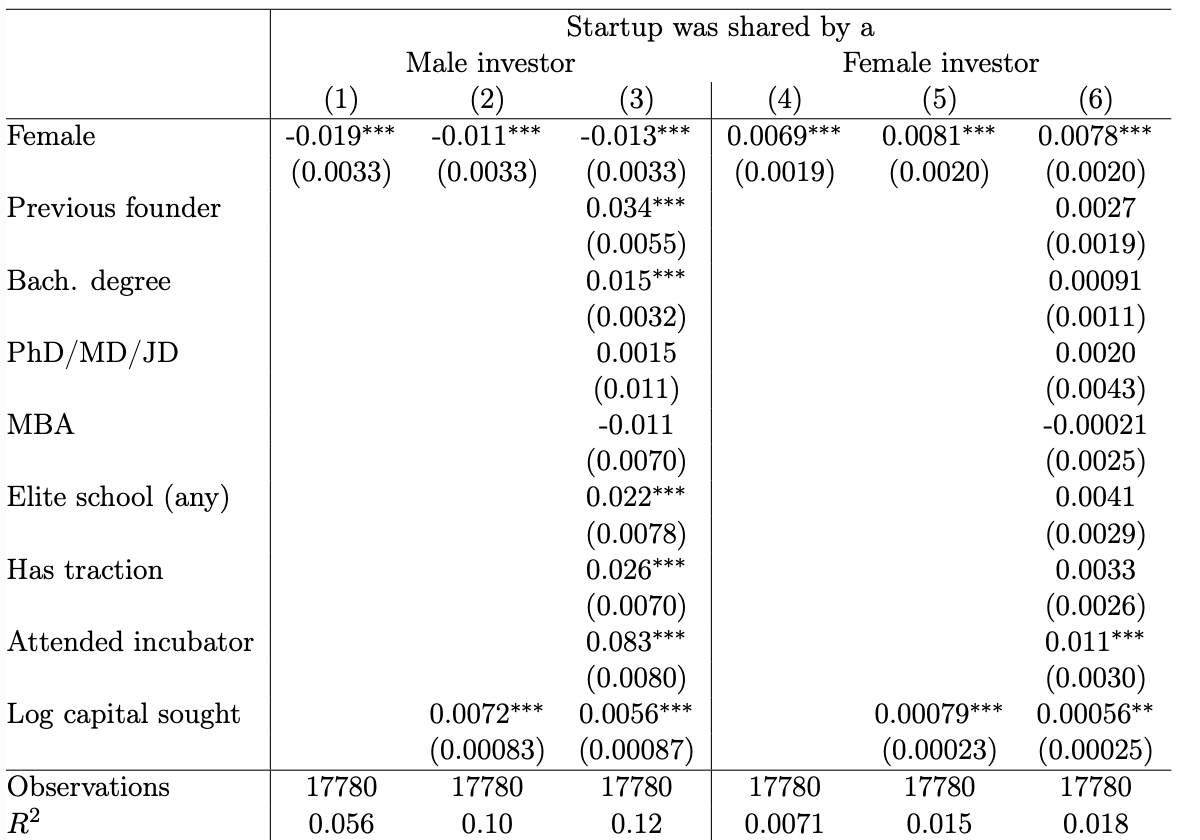

We study whether early stage investors have gender biases using a proprietary dataset from An- gelList that allows us to observe private interactions between investors and fundraising startups. We find that male investors express less interest in female entrepreneurs compared to observably similar male entrepreneurs. In contrast, female investors express more interest in female entrepreneurs. These findings do not appear to be driven by within-gender screening/monitoring advantages or gender differences in risk preferences. Moreover, the male-led startups that male investors express interest in do not outperform the female-led startups they express interest in—they underperform. Overall, the evidence is consistent with gender biases.

2018, Review of Financial Studies

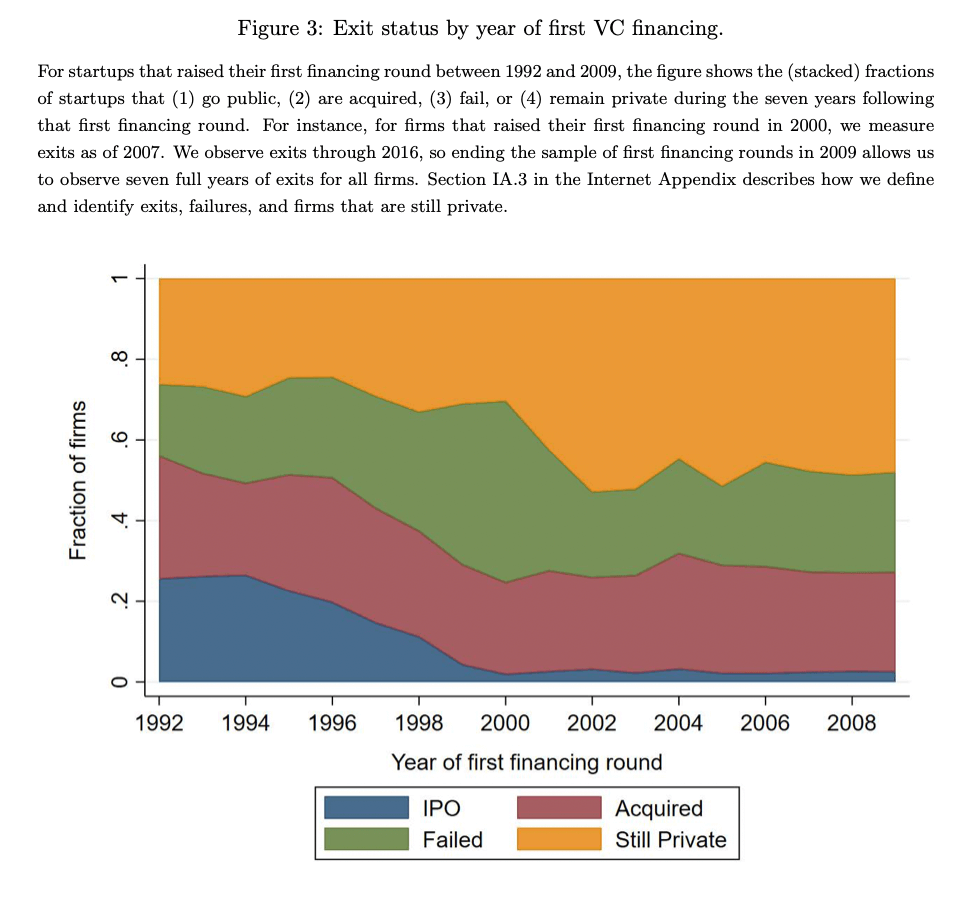

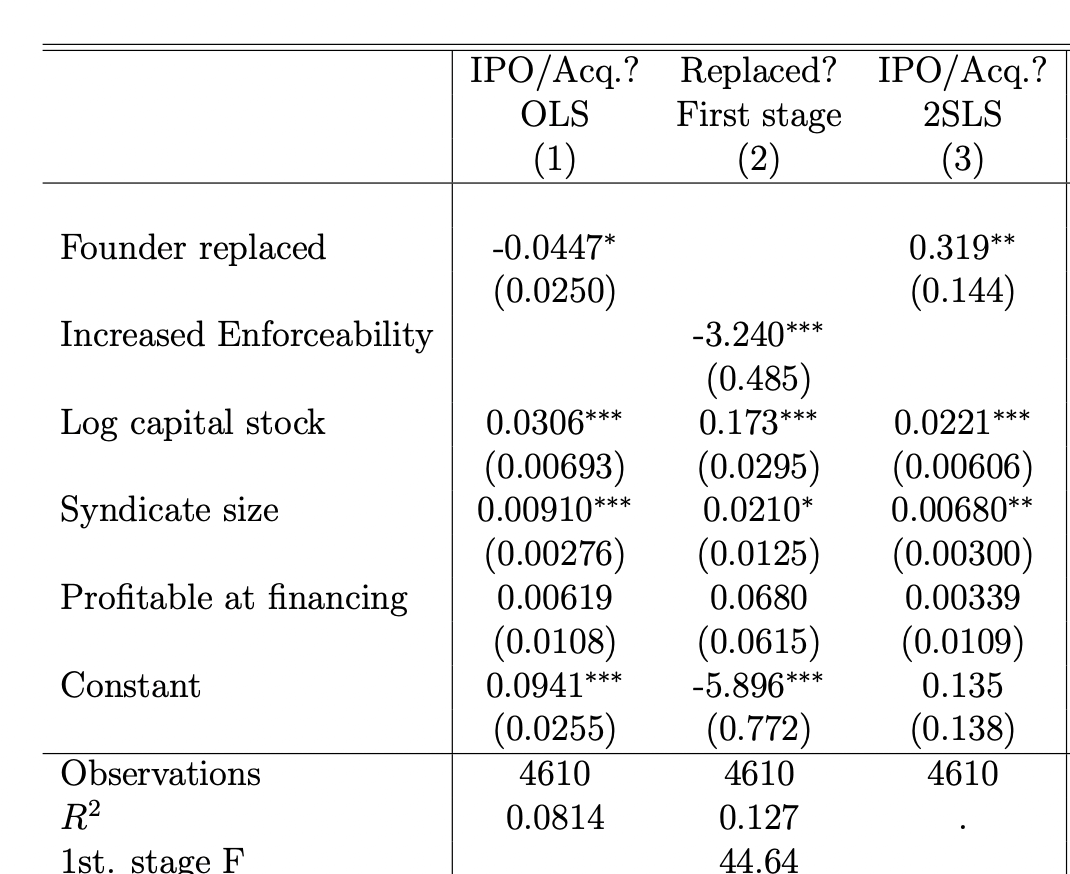

We provide causal evidence that venture capitalists (VCs) improve the performance of their portfolio companies by replacing founders. Using a database of venture capital financings augmented with hand-collected founder turnover events, we exploit shocks to the supply of outside executives via 14 states’ changes to non-compete laws from 1995 to 2016. Naive regressions of startup performance on replacement suggest a negative correlation that may reflect negative selection. Indeed, instrumented regressions reverse the sign of this effect, suggesting that founder replacement instead improves performance. The evidence points to the replacement of founders as a specific mechanism by which VCs add value.

2017, Journal of Financial Economics

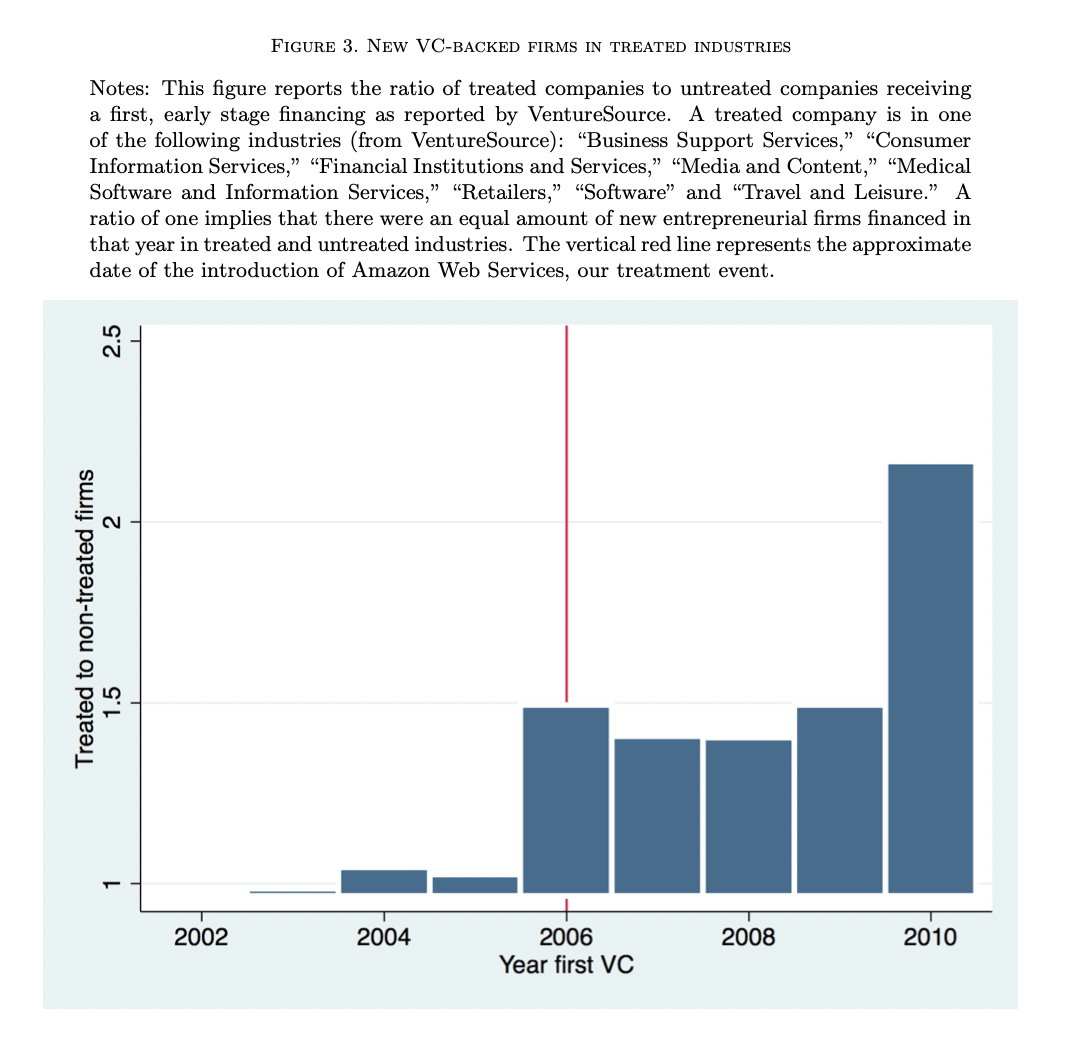

We study how technological shocks to the cost of starting new businesses have led the venture capital model to adapt in fundamental ways over the prior decade. We both document and provide a framework to understand the changes in the investment strategy of venture capitalists (VCs) in recent years – an increased prevalence of a “spray and pray” investment approach – where investors provide a little funding and limited governance to an increased number of startups that they are more likely to abandon, but where initial experiments significantly inform beliefs about the future potential of the venture. This adaptation and related entry by new financial intermediaries has led to a disproportionate rise in innovations where information on future prospects is revealed quickly and cheaply, and reduced the relative share of innovation in complex technologies where initial experiments cost more and reveal less.

2017, Management Science

With:

Indraneel Chakraborty (Univ. of Miami)

2015, Journal of Finance

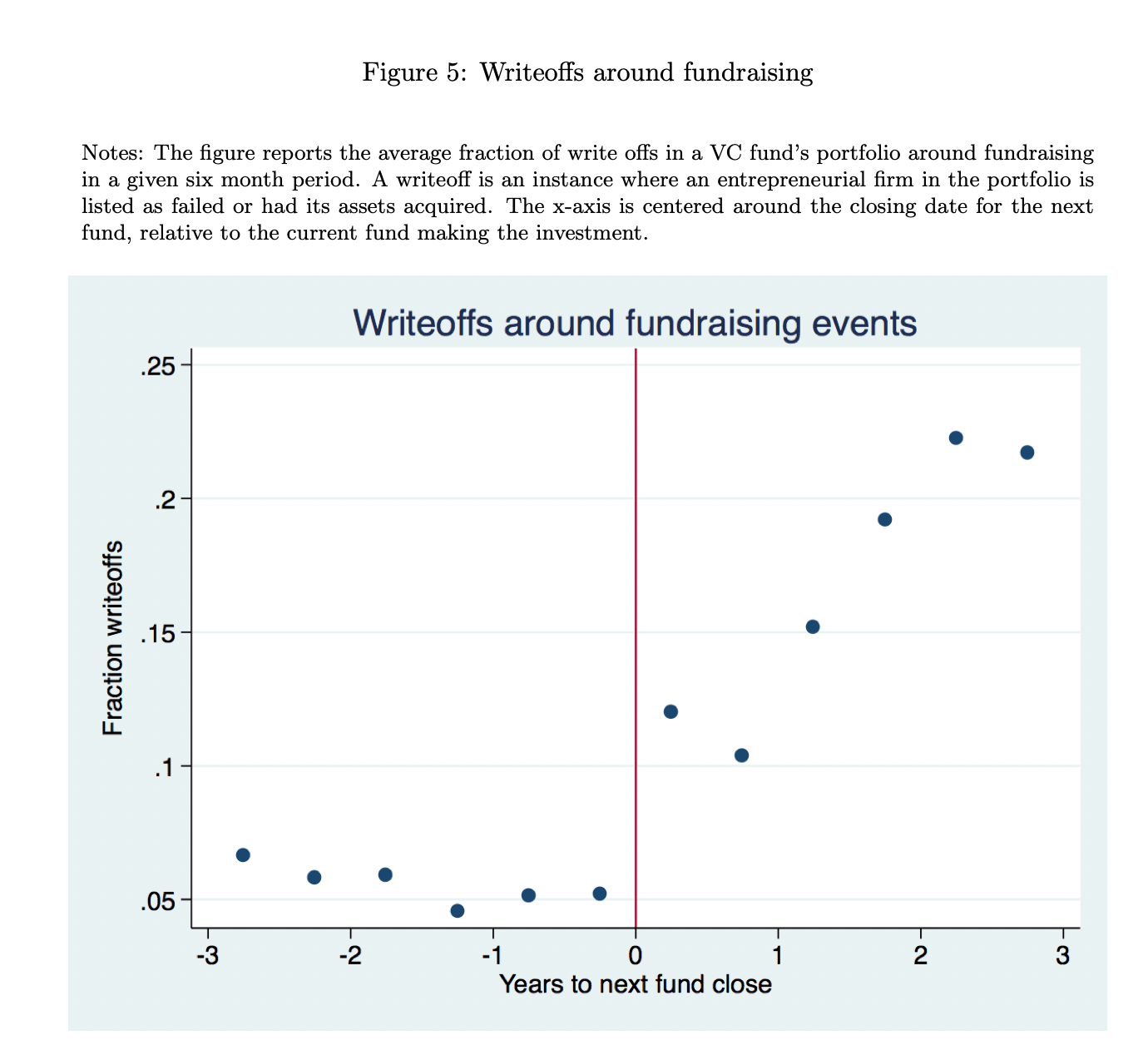

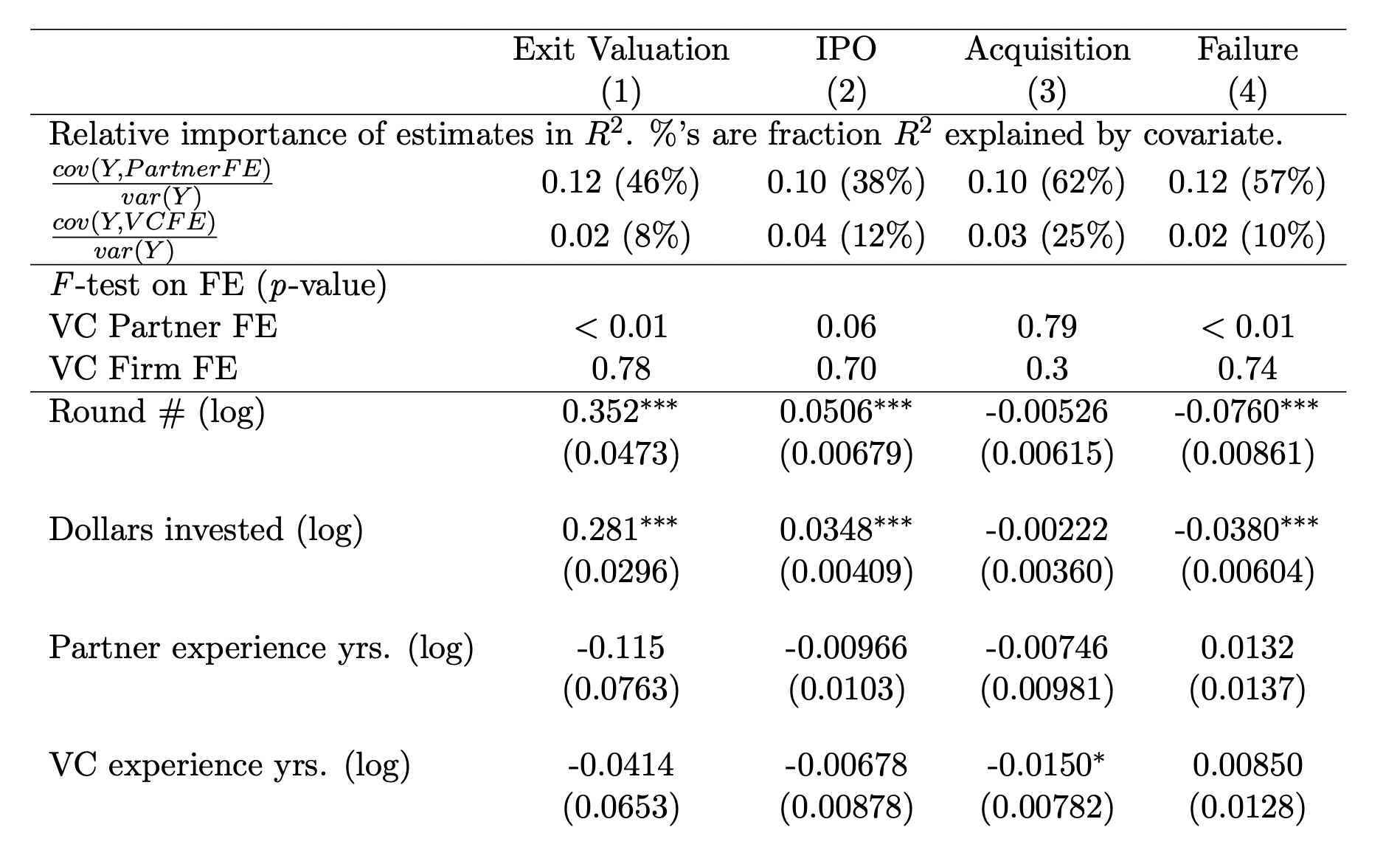

This paper investigates whether individual venture capitalists have repeatable investment skill and the extent to which their skill is impacted by the venture capital (VC) firm where they work. We examine a unique data set that tracks the performance of individual venture capitalists’ investments over time and as they move between firms. We find evidence of skill and exit style differences even among venture partners investing at the same VC firm at the same time. Furthermore, our estimates suggest the partners’ human capital is two to five times more important than the VC firm’s organizational capital in explaining performance.

2014, Review of Economics and Statistics

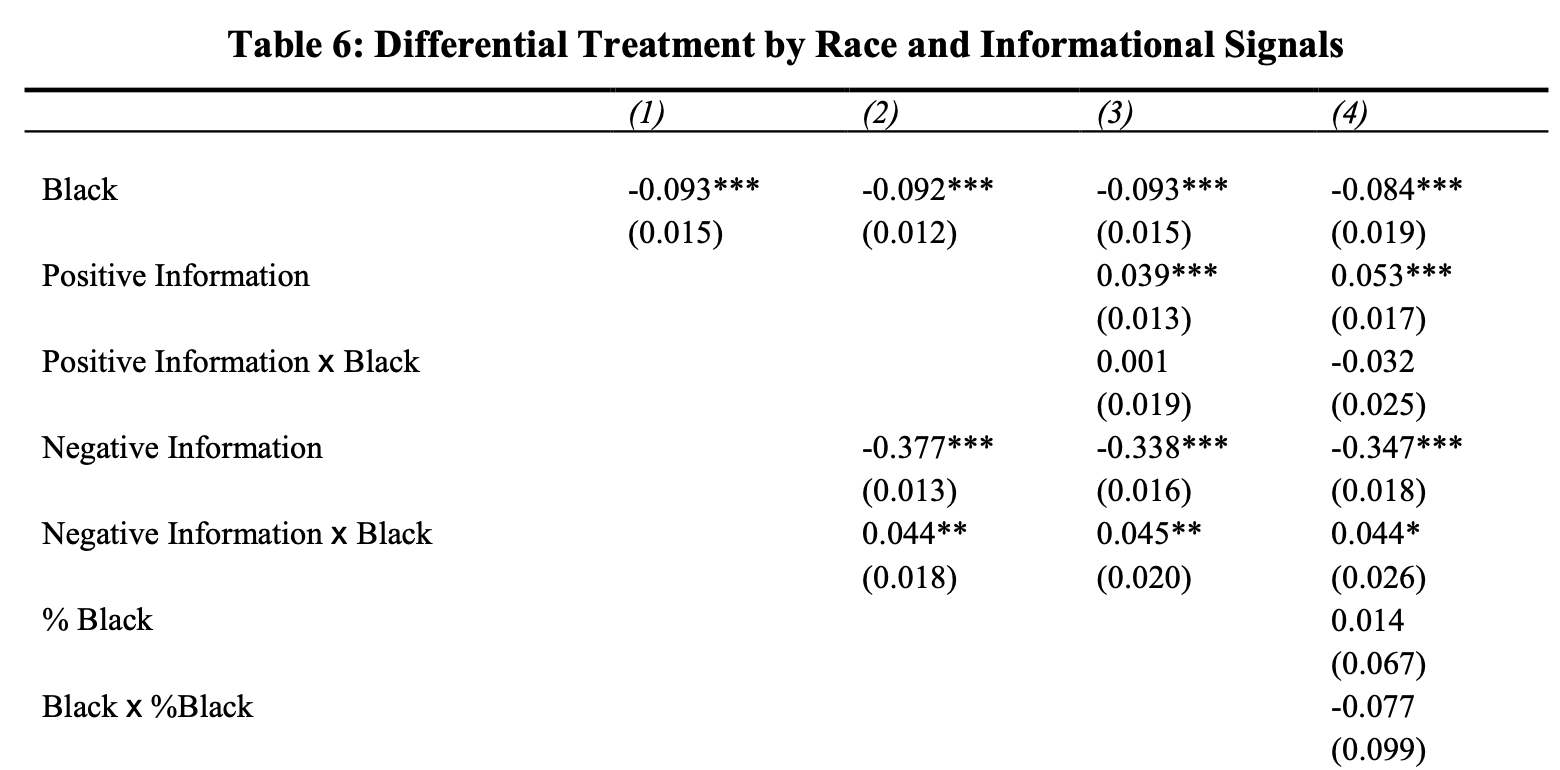

A model of racial discrimination provides testable implications for two features of statistical discriminators: differential treatment of signals by race and heterogeneous experience that shapes perception. We construct an experiment in the U.S. rental apartment market that distinguishes statistical discrimination from taste-based discrimination. Responses from over 14,000 rental inquiries with varying applicant quality show that landlords treat identical information from applicants with African-American and white sounding names differently. This differential treatment varies by neighborhood racial composition and signal type in a manner consistent with statistical discrimination and in contrast to patterns predicted by a model of taste-based discrimination.

2013, Review of Financial Studies

With:

Charles Jones (Columbia) and Matthew Rhodes-Kropf (MIT)

This paper demonstrates how the principal-agent problem between venture capitalists and their investors (limited partners) causes limited partner returns to depend on diversifiable risk. Our theory shows why the need for investors to motivate VCs alters the negotiations between VCs and entrepreneurs and changes how new firms are priced. The three-way interaction rationalizes the use of high discount rates by VCs and predicts a correlation between total risk and net of fee investor returns. We take our theory to a unique data set and find empirical support for the effect of the principal-agent problem on equilibrium private equity asset prices.